Household debt, consumption and wealth, by Ilian Mihov:

It is very common these days to hear that the global economy has no way of recovering because the most powerful engine of global demand – the American consumer – is choking in debt. ...

Indeed,... debt stands at $14.068 trillion or slightly less than 100% of GDP. Does this mean that the economy is doomed? There are two points that one has to take into account when evaluating the role of household debt in the economy.

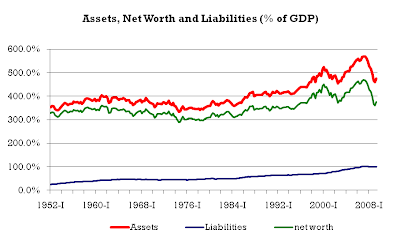

1. Debt is only one side of the story. Households also own assets. Consumption is a function of (net) wealth, not only of indebtedness. Up to a first approximation what matters is the difference between assets and liabilities. Indeed, no one thinks that a person with $10 million in debt is going to cut his or her consumption, if you know that this person has $10 billion in assets. So, how do American consumers fare in terms of net worth? Below is a graph with three ratios – assets-to-GDP, debt-to-GDP and net-worth-to-GDP. Although household debt stands at 100% of GDP, assets owned by US households currently stand at $67.2 trillion or 475% of GDP. The net worth of the American households is estimated to be over 375% of GDP.

Are these assets sufficient? This is hard to tell because theory does not provide convincing guidance as to what the wealth-to-GDP ratio should be. But we can look at the data to see how these numbers compare to historical averages. The average ratio of US household net worth from 1952Q1 to 2009Q2 is about 350% (if we exclude the two bubbles, the ratio is 330%). In short, US households today have more net wealth than they had in normal times in the post WWII period. Contrary to all complaints, US households today are richer than at any point in time in the pre-1995 period (and again, this is relative to GDP; in absolute terms no one will be surprised that this statement is true).

But maybe it is the composition of debt that matters – people today live off their credit cards. It turns out that consumer credit has increased indeed over the past 20 years but the numbers are not shocking. From about 14% in 1990, consumer credit rose to 17.3% in 2009 (again the numbers are relative to GDP). ...

2. Even if we concede that debt can reduce consumption for an individual, it is a bit trickier to make the same argument for the national economy. The reason is that the liability of one individual is an asset for someone else. In the graph above, the thin blue line is in fact included in the thick red line! ...

There are ways in which this “neutrality of debt” may break down. For example, if those who are indebted have a higher propensity to consume than the lenders, then debt will lead them to cut their consumption by more than the lenders will increase theirs (due to the wealth effect). This is possible and even plausible, but it is not clear whether empirically this effect is significant. Second, it might be that household debt is held by foreigners. Again, the data are not very supportive of this hypothesis because the net foreign asset position of the US is not (yet) devastating – less than 20% of GDP.

In general, many other “imperfections” in the market economy can result in the importance of debt for aggregate consumption, and I do agree that some of these imperfections are realistic and important. The main point of the argument is that we need a more nuanced view of why debt matters. We should keep in mind that the net worth of US households is still quite high (375% of GDP) and that debt should be viewed from a general equilibrium point of view and not only in absolute terms.